Defence Finance Monitor Digest #61

Defence Finance Monitor is a specialised source of analysis for professionals who seek to anticipate how strategic priorities shape investment patterns in the defence sector. In a landscape shaped by high-stakes political choices and rapid technological shifts, understanding the link between military doctrine, operational requirements, and industrial policy is not a competitive edge—it is a prerequisite.

We analyse how strategic imperatives set by NATO, the European Union, allied Indo-Pacific democracies, and national Ministries of Defence translate into procurement programmes, innovation roadmaps, and long-term industrial priorities. Rather than listing individual companies, we track how clearly defined strategic challenges—such as deterrence gaps, technological dependencies, or capability shortfalls—are converted into funding schemes and institutional demand. Only companies that respond to these challenges become relevant to institutional buyers and, by extension, to investors. This framework has already enabled a growing community of analysts and financial professionals to make more consistent, risk-aware decisions and to avoid costly misalignments.

Building on this methodology, we are developing a structured database of companies analysed and classified according to the strategic-technological criteria set out in our framework. Subscribing to Defence Finance Monitor therefore provides not only access to in-depth reports, but also to a continuously expanding database of European and allied defence firms assessed against clear benchmarks. Each company is positioned according to its alignment with EU and NATO priority capability areas, its contribution to European strategic autonomy, its level of interoperability and deterrence value, and its role in reducing dependencies on non-allied suppliers. Classification also covers technology readiness levels, participation in EU and NATO programmes, intellectual property assets, and dual-use applications. This allows subscribers to compare, benchmark, and identify the most strategically relevant actors within a coherent, transparent, and decision-oriented taxonomy.

Subscribing to Defence Finance Monitor means gaining access to a strategic intelligence service that connects financial decisions with defence priorities. At the core of our work is a structured database of European and allied defence companies, classified according to strategic-technological criteria such as autonomy, interoperability, deterrence, and supply chain resilience. In today’s environment, profitable investment requires more than market data: it requires understanding how limited public resources are channelled toward specific capability gaps, sovereign technologies, and the reduction of non-allied dependencies. By combining in-depth reports with a continuously expanding company database, Defence Finance Monitor enables investors to anticipate demand, benchmark firms against institutional priorities, and avoid costly misalignments.

European Defence: From Emergency Measures to Structural Readiness by 2030

Europe is undergoing a profound transformation in its approach to security and defence planning. In the immediate aftermath of Russia’s invasion of Ukraine, governments responded with emergency measures, raising defence budgets at unprecedented speed and replenishing depleted stockpiles of ammunition and equipment. These initial actions were necessary, yet they were fragmented and crisis-driven, designed to address urgent shortfalls rather than long-term needs. Over time, the limitations of this reactive approach became clear, pushing European leaders to seek a more permanent solution. The emerging framework, described as the “road to readiness 2030,” shifts the focus from temporary rearmament to a stable and predictable defence posture. The concept entails strengthening the industrial base, building resilient supply chains, harmonising procurement rules, and ensuring that production translates into deployable capabilities. For the investment community, this transition signals the emergence of durable visibility in defence spending, an environment where long-term contracts, cross-border initiatives, and dual-use infrastructure become central features of Europe’s economic and strategic landscape.

ICEYE Demonstrates Tactical ISR Cell at NATO Tiger Meet 2025

On 26 September 2025, ICEYE, a Finland-based space company classified as a scale-up and mid-cap player in the synthetic aperture radar (SAR) segment, announced the operational demonstration of its new ISR Cell during the NATO Tiger Meet exercise in Beja, Portugal. The exercise, involving 1,700 personnel from 12 NATO members, provided an international setting for testing interoperability and joint tactics. ICEYE’s participation represented the first time a commercial space-SAR operator outside the circle of traditional prime contractors showcased an end-to-end ISR capability in a NATO multinational exercise. For a firm established as a venture-backed startup and now consolidating its industrial role, the demonstration constitutes a symbolic milestone: it indicates not only technological maturity, but also recognition of tactical relevance by NATO forces. The event follows a sequence of September announcements on the launch of ICEYE’s fourth-generation SAR satellites, contracts with national defence institutions, and direct service agreements with NATO bodies, highlighting a robust pipeline of institutional demand for tactical space-based intelligence.

InvestEU Reform: Simplification, Guarantee Expansion and Strategic Relevance

The political agreement reached on 23 September 2025 between the Council and the European Parliament marks a significant recalibration of the InvestEU framework, designed to strengthen competitiveness while extending the programme’s reach to strategic domains such as defence industrial policy and military mobility. For years, InvestEU has functioned as the Union’s flagship investment platform, blending public guarantees with private capital to mobilise large-scale financing. The new deal, embedded in the Omnibus II package, seeks to eliminate administrative complexity and unlock greater investment potential. It does so by raising the EU guarantee, aligning InvestEU with the competitiveness agenda laid out in the Draghi and Letta reports, and embedding support for critical sectors, including clean industry and defence. This reflects a wider recognition that competitiveness, security and industrial policy are now inseparable in Europe’s financial governance.

EIB Group Approves €7.1 Billion for Technology, Energy Security, Defence and Ukraine

The European Investment Bank Group has approved a package of €7.1 billion in new financing that marks an expansion of its role as the Union’s long-term industrial lender into strategically sensitive domains. Traditionally the EIB focused on infrastructure, climate, and cohesion, but the September 2025 decisions demonstrate how the institution is embedding defence and dual-use into its financing architecture. The allocations span European technology leadership, life sciences, energy security, and urban development, while explicitly including security and defence projects. Importantly, the measures extend beyond internal EU priorities to external engagements, notably Ukraine, where the EIB is already a central conduit for emergency reconstruction and resilience investment. This decision must be read in the broader context of the EU’s attempt to operationalise strategic autonomy by blending public guarantees, private capital mobilisation, and institutional lending under a single policy umbrella.

Europe’s First Private Credit Fund for Defence SMEs

The establishment of a dedicated financial instrument targeting the European defence sector marks a significant institutional development in the intersection between security policy and capital markets. For decades, European defence has been financed primarily through government budgets, complemented by limited private equity and occasional industrial partnerships. The creation of Sienna Hephaistos Private Investments, with the European Investment Fund acting as cornerstone investor, demonstrates a structural shift toward the mobilisation of private debt to reinforce the industrial base. The logic underpinning this initiative is rooted in the recognition that Europe’s security cannot depend solely on public expenditure or reliance on non-European suppliers. Instead, there is an urgent need to broaden the spectrum of financing channels available to small and mid-sized firms that constitute the backbone of the defence value chain. This development takes place against the background of heightened geopolitical instability, the pressure to accelerate rearmament, and the emergence of strategic autonomy as a guiding European principle.

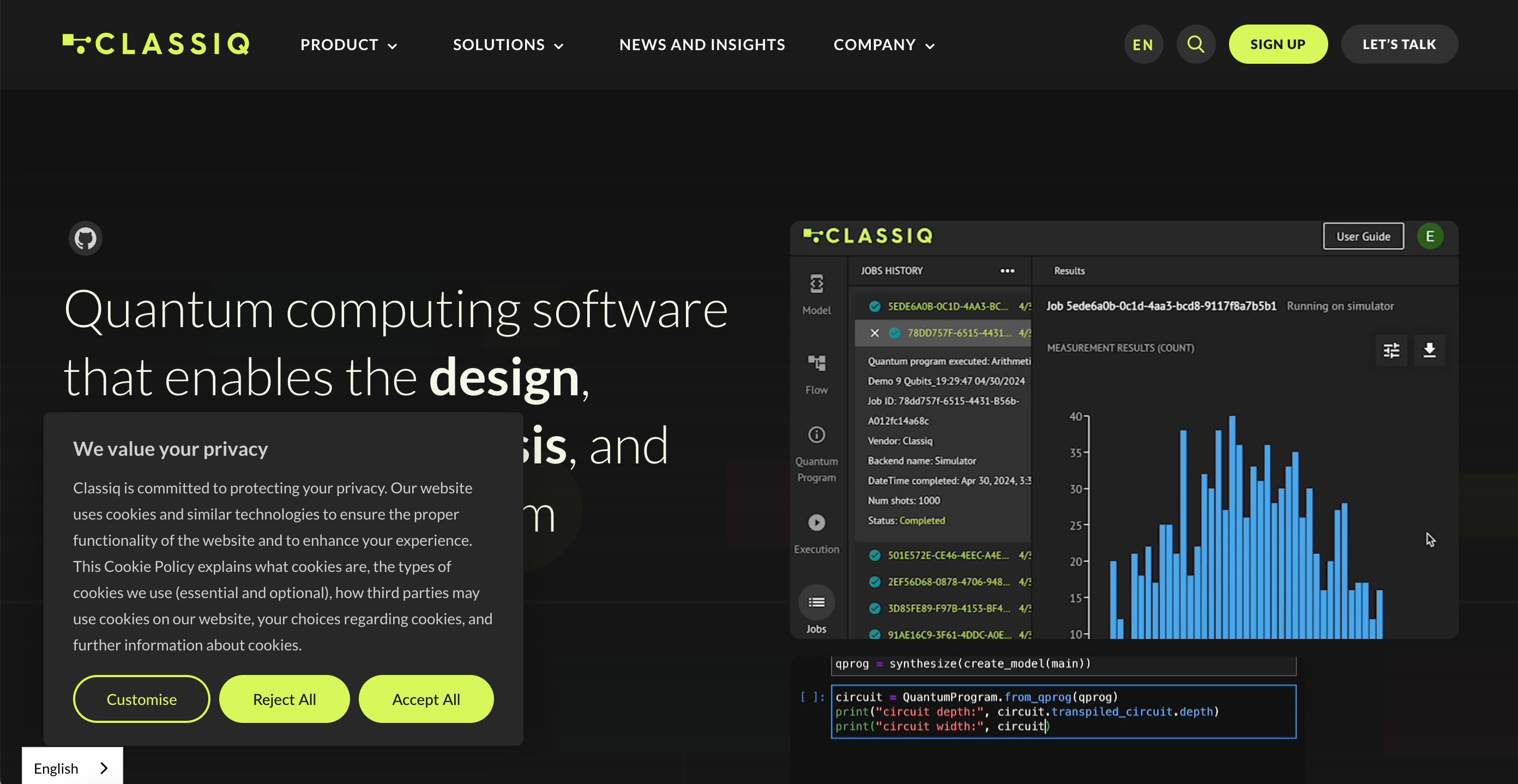

Classiq (Israel) – Strategic-Technological Analysis

Classiq is an Israeli quantum computing software company founded to accelerate the design of quantum algorithms. Its platform translates high-level descriptions of computation into optimized quantum circuit implementations. In an era where Europe and NATO seek to harness emerging technologies for defense, Classiq’s tools are relevant to European ambitions in quantum computing and cyber resilience. This analysis explores Classiq’s corporate profile, technologies, and strategic fit with European defense priorities. It examines how Classiq’s capabilities might enhance interoperability and deterrence while reducing dependencies on non-allied suppliers. The report is intended for defense planners and analysts interested in deep-tech companies and European strategic autonomy.

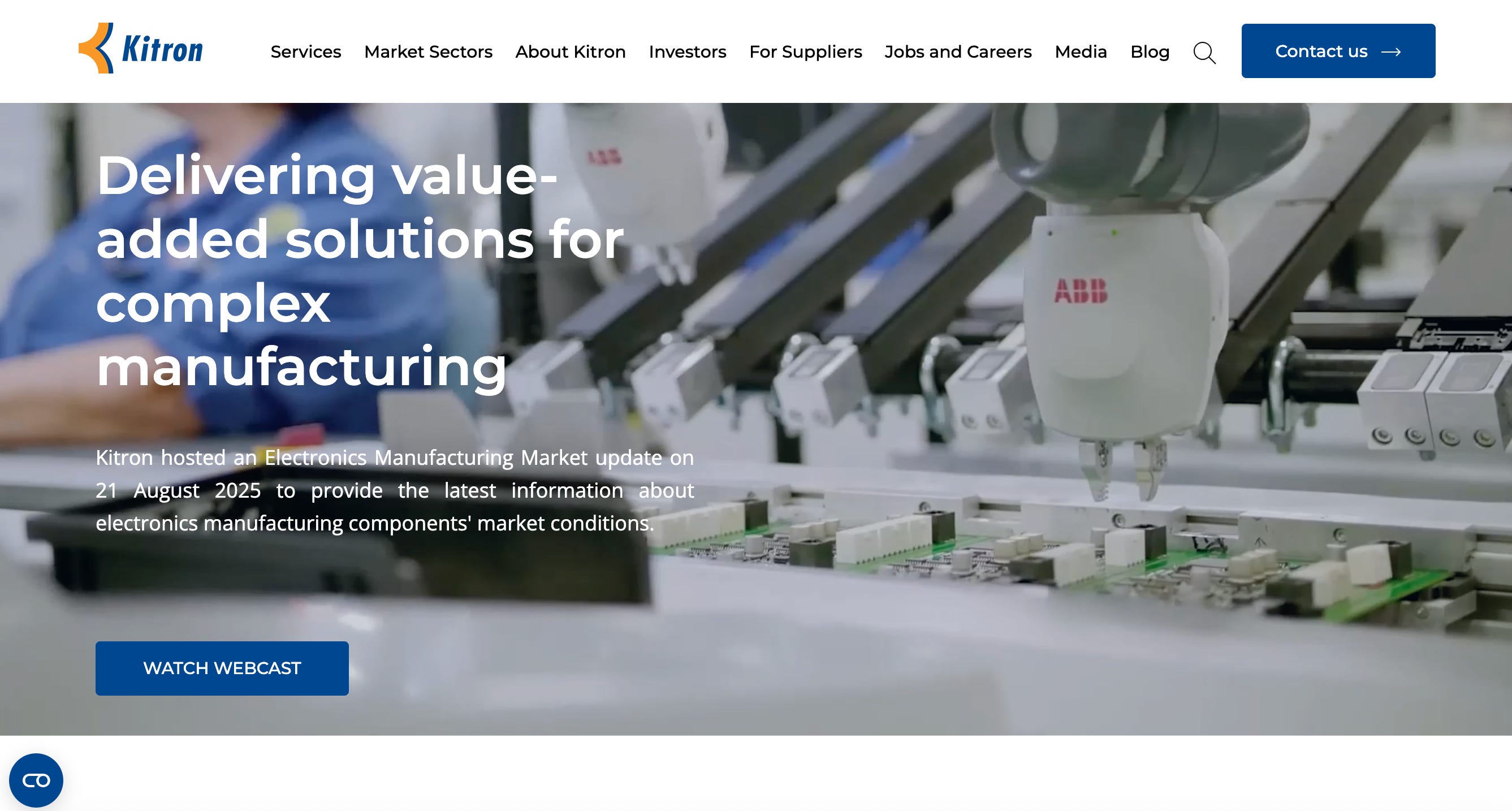

Kitron ASA: A Strategic Electronics Partner for European Defense Autonomy

In an era where Europe seeks to reclaim control over critical defense technologies, one lesser-known firm has quietly become indispensable. Kitron ASA is a Scandinavian electronics manufacturer powering some of NATO’s most advanced systems – from the F-35 stealth fighter’s communications modules to next-generation naval missiles[1][2]. Headquartered in Norway, Kitron builds the “brains” inside radars, encrypted networks, and autonomous drones, positioning itself as a behind-the-scenes linchpin of European defense innovation. While not a household name, Kitron’s growing order backlog and rapid expansion in defense electronics signal its rising strategic profile. The company has leveraged surging European defense budgets and a renewed focus on supply-chain sovereignty to secure high-value contracts in radar systems, missile guidance, and unmanned aerial vehicles[3]. With production anchored in Europe – including new facilities in Norway and the Czech Republic – Kitron offers EU and NATO partners a trusted, on-continent alternative to offshore electronics suppliers. As defense spending hits historic highs and Europe strives to reduce dependency on non-allied sources, Kitron’s role in enabling indigenous capabilities has never been more critical. This report provides a comprehensive analysis of Kitron ASA’s strategic-technological positioning, examining how this mid-cap EMS (Electronics Manufacturing Services) provider contributes to European strategic autonomy, NATO interoperability, and the reduction of risky dependencies in the defense supply chain.

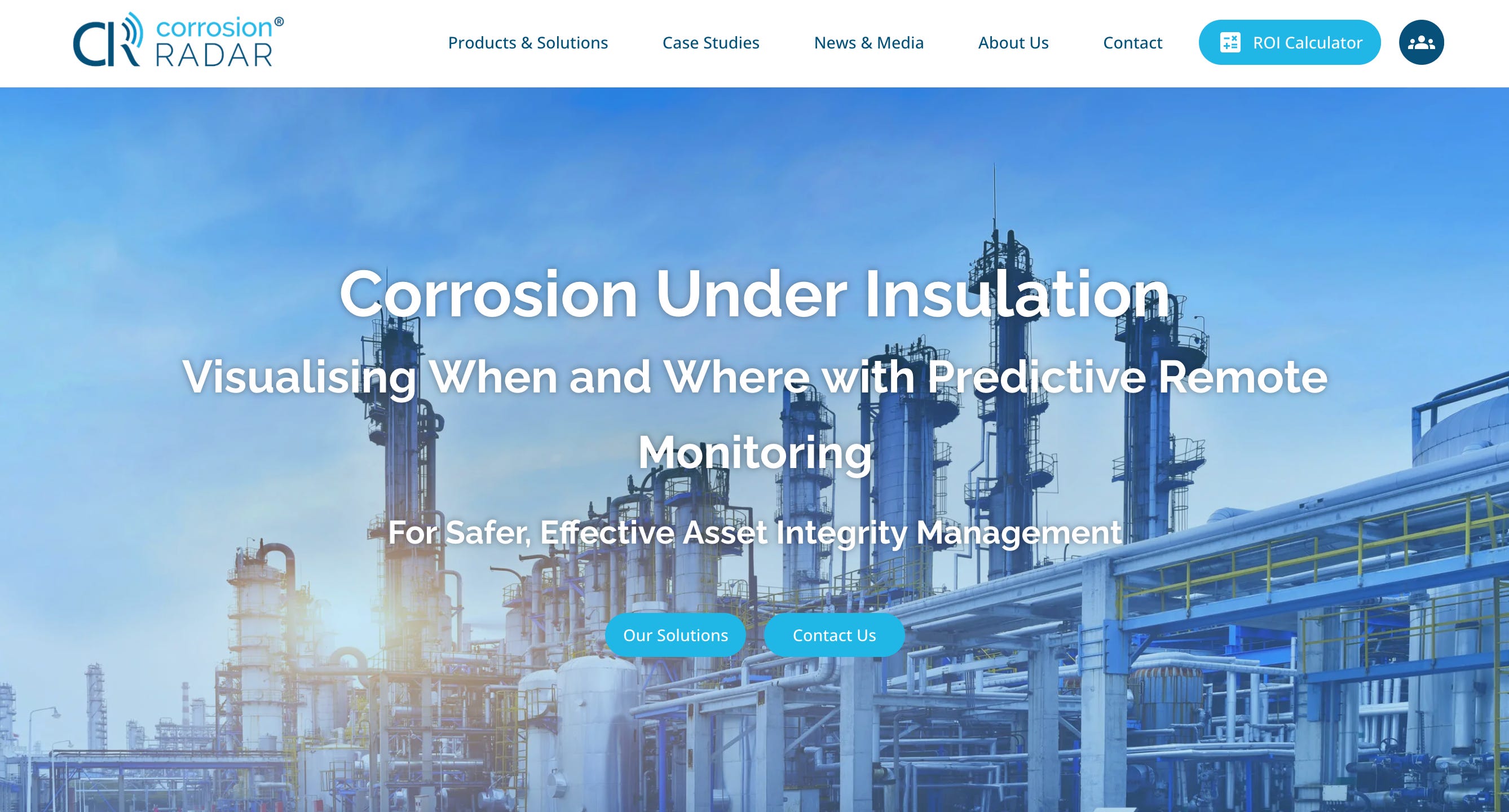

CorrosionRADAR (Cranfield University, UK) – Strategic-Technological Analysis

Developed from a Cranfield University research project, CorrosionRADAR is a UK-based deep-tech startup that aims to transform how critical infrastructure corrosion is monitored. Modern European energy networks span vast pipelines, often in hazardous or hard-to-reach environments, where manual inspections are slow, costly and expose workers to risk[1]. CorrosionRADAR adapts space-grade electromagnetic sensing for continuous remote inspection of pipelines and insulated tanks. Its patented “waveguide” sensors are embedded under insulation and linked to an analytics platform, enabling operators to detect and even predict corrosion under insulation (CUI) without removing pipe cladding[2][3]. This analysis examines CorrosionRADAR’s profile through the lens of European defense-industrial strategy: a UK-origin technology with clear civil safety uses that may also bolster energy and defense infrastructure security. We assess its legal and corporate identity, technology assets and readiness, program affiliations, and industrial partnerships to judge how the company supports European strategic autonomy, NATO interoperability and supply-chain resilience. Key questions include whether a European (allied) supplier can use this innovation to replace non-allied alternatives, contribute to multi-domain defense operations, and enhance deterrence by protecting critical energy assets. The following report will detail CorrosionRADAR’s activities and technologies, providing an objective view of its strategic value to Europe