Defence Finance Monitor Digest #55

Defence Finance Monitor is a specialised source of analysis for professionals who seek to anticipate how strategic priorities shape investment patterns in the defence sector. In a landscape shaped by high-stakes political choices and rapid technological shifts, understanding the link between military doctrine, operational requirements, and industrial policy is not a competitive edge—it is a prerequisite.

We analyse how strategic imperatives set by NATO, the European Union, allied Indo-Pacific democracies, and national Ministries of Defence translate into procurement programmes, innovation roadmaps, and long-term industrial priorities. Rather than listing individual companies, we track how clearly defined strategic challenges—such as deterrence gaps, technological dependencies, or capability shortfalls—are converted into funding schemes and institutional demand. Only companies that respond to these challenges become relevant to institutional buyers and, by extension, to investors. This framework has already enabled a growing community of analysts and financial professionals to make more consistent, risk-aware decisions and to avoid costly misalignments.

Building on this methodology, we are developing a structured database of companies analysed and classified according to the strategic-technological criteria set out in our framework. Subscribing to Defence Finance Monitor therefore provides not only access to in-depth reports, but also to a continuously expanding database of European and allied defence firms assessed against clear benchmarks. Each company is positioned according to its alignment with EU and NATO priority capability areas, its contribution to European strategic autonomy, its level of interoperability and deterrence value, and its role in reducing dependencies on non-allied suppliers. Classification also covers technology readiness levels, participation in EU and NATO programmes, intellectual property assets, and dual-use applications. This allows subscribers to compare, benchmark, and identify the most strategically relevant actors within a coherent, transparent, and decision-oriented taxonomy.

Subscribing to Defence Finance Monitor means gaining access to a strategic intelligence service that connects financial decisions with defence priorities. At the core of our work is a structured database of European and allied defence companies, classified according to strategic-technological criteria such as autonomy, interoperability, deterrence, and supply chain resilience. In today’s environment, profitable investment requires more than market data: it requires understanding how limited public resources are channelled toward specific capability gaps, sovereign technologies, and the reduction of non-allied dependencies. By combining in-depth reports with a continuously expanding company database, Defence Finance Monitor enables investors to anticipate demand, benchmark firms against institutional priorities, and avoid costly misalignments.

The Economics of Urban Combat: Sustaining Demand for Infantry Systems

Urban combat remains one of the most decisive features of contemporary conflict, but its significance goes well beyond tactics. For defence industries and investors, it represents a consistent and predictable source of demand, as no technological revolution has removed the need for physical control of territory. Cities, with their density of infrastructure and population, continue to impose requirements that cannot be satisfied by stand-off fires alone. This means that states must continually procure equipment and systems specifically designed for close combat, ensuring that the market for protective gear, portable communications, and short-range weapons remains structurally resilient. Unlike large platforms that may be acquired in cycles of decades, urban warfare drives recurring procurement in shorter cycles, generating continuous opportunities for industry and finance. The financial implication is clear: as long as cities remain central to conflict, so too will steady flows of investment into infantry systems.

Drones and the Reshaping of Close Combat Firepower

The widespread use of drones and loitering munitions has fundamentally altered the economics and dynamics of close combat. What began as a niche capability has become a core driver of procurement priorities across modern armed forces. Lightweight, portable, and relatively inexpensive, drones provide tactical units with surveillance and precision-strike capabilities that once required costly platforms. For industry and finance, this shift is significant: the demand for small unmanned systems is recurring, resilient, and growing, as no army can afford to operate without them. Unlike long-range systems procured in decades-long cycles, drones follow shorter, high-turnover procurement paths, ensuring constant revenue streams. Defence investors should recognize that the rise of drones has created a structural market segment, less visible than fighter jets or tanks but increasingly central to sustained military spending.

Company Profiles & Industrial Intelligence

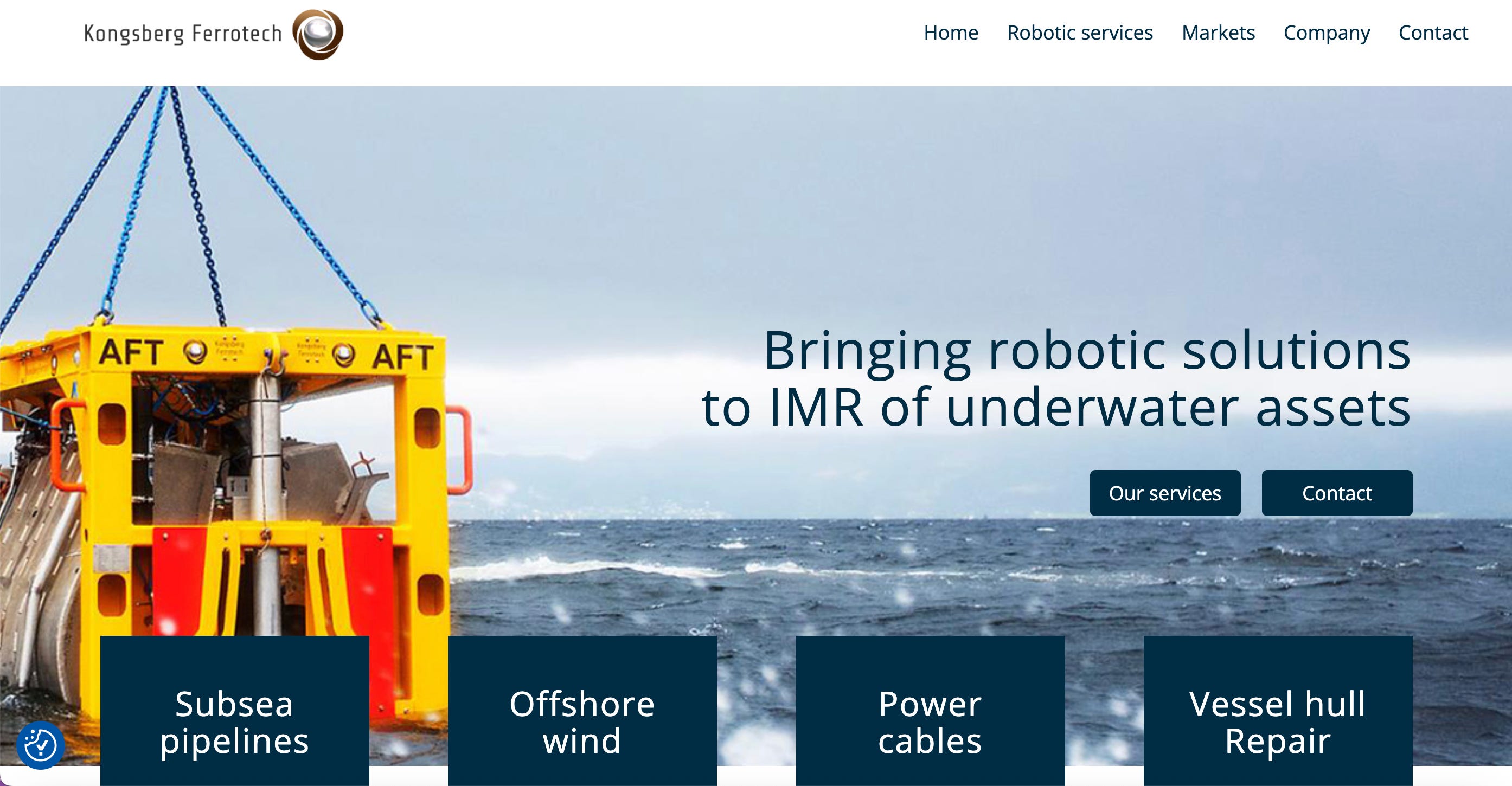

Kongsberg Ferrotech: Subsea Robotics for Europe’s Critical Infrastructure Security

Kongsberg Ferrotech is a Norwegian deep-tech innovator specializing in robotic inspection, maintenance and repair (IRM) of underwater infrastructure. Its flagship robotic platform, Nautilus, creates a localized “dry habitat” around subsea assets, enabling in-situ repairs of pipelines, power cables, vessel hulls and offshore renewable foundations that would otherwise require costly dry-docking or intervention by divers[1][2]. This capability directly addresses European concerns over the security and resilience of critical undersea infrastructure – from energy pipelines to fiber-optic data cables – which have been highlighted as vulnerable strategic assets by NATO and EU policymakers[3][2]. In mid-2025 Kongsberg Ferrotech raised a €12 million seed round led by NATO’s Innovation Fund and Norway’s Investinor[4][5], underscoring its relevance to alliance-level priorities. This report explores how Ferrotech’s technology portfolio and strategic positioning contribute to European strategic autonomy, deterrence, and supply-chain resilience in the defense and dual-use domain.

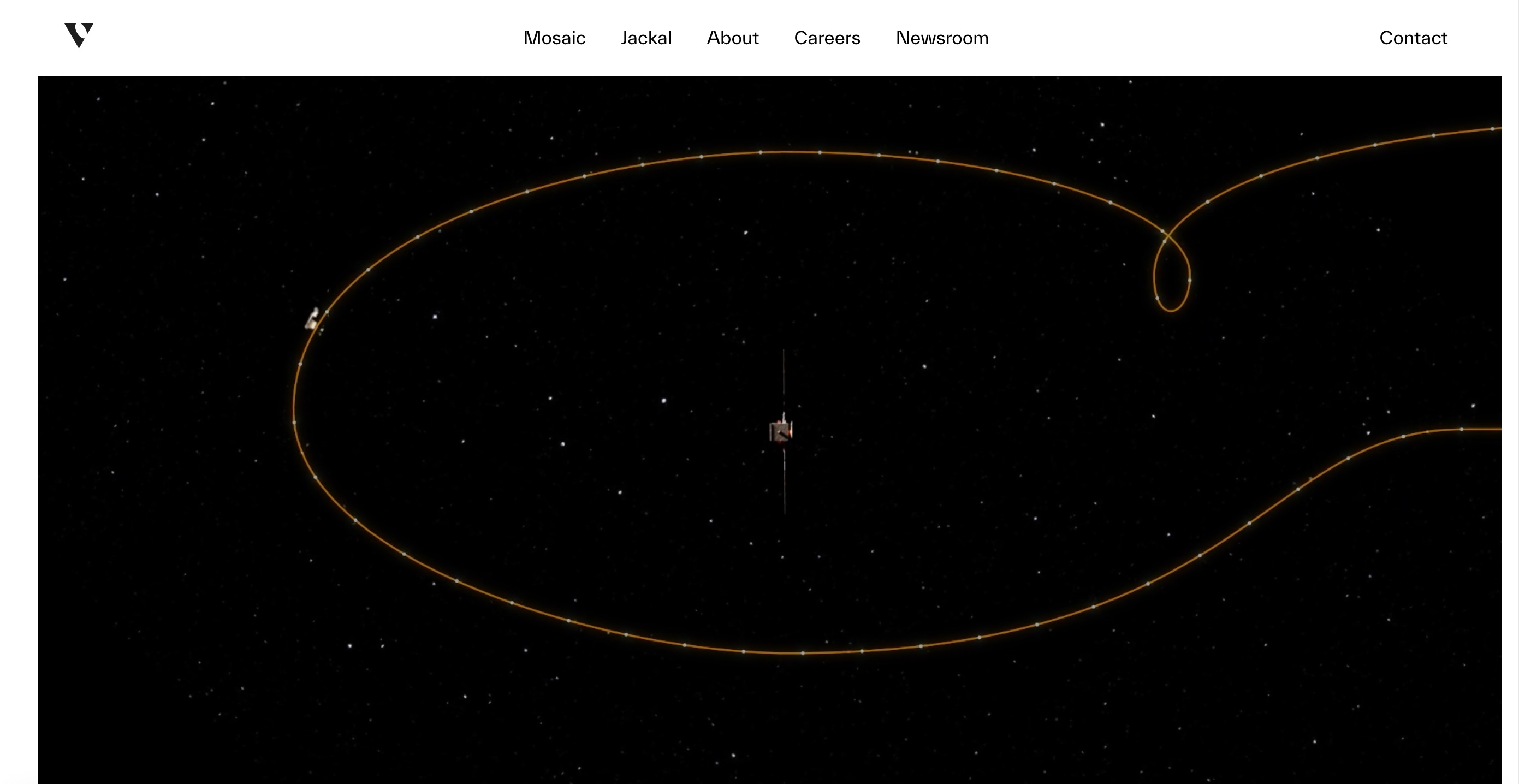

True Anomaly — European Strategic-Technological Analysis

Europe is rapidly expanding its efforts to secure strategic autonomy in space, recognizing that space-based assets undergird modern economies and security. This report examines True Anomaly, a U.S. space-defense technology firm, to explore how its offerings intersect with Europe’s objectives for resilient space capabilities. True Anomaly, founded in 2022 in Colorado, develops spacecraft and software for space domain awareness and autonomous operations[1][2]. Its flagship products – a spacecraft operating system (Mosaic) and an autonomous orbital vehicle (Jackal) – are designed to track space objects, collect data, and even rendezvous with other satellites for imaging[3][2]. Such capabilities clearly serve the U.S. and allied defense communities (e.g. U.S. Space Force contracts) but raise questions for Europe’s own strategic autonomy: could these technologies bolster European deterrence or do they create new dependencies? Given recent EU initiatives like the EU Space Act to harmonize space sovereignty[4][5] and NATO’s recognition that space is an operational domain linked to deterrence[6], understanding True Anomaly’s portfolio is crucial. The following analysis profiles the company’s structure, technologies, and strategic role, focusing on how (and whether) its assets align with European defense and space policy goals.

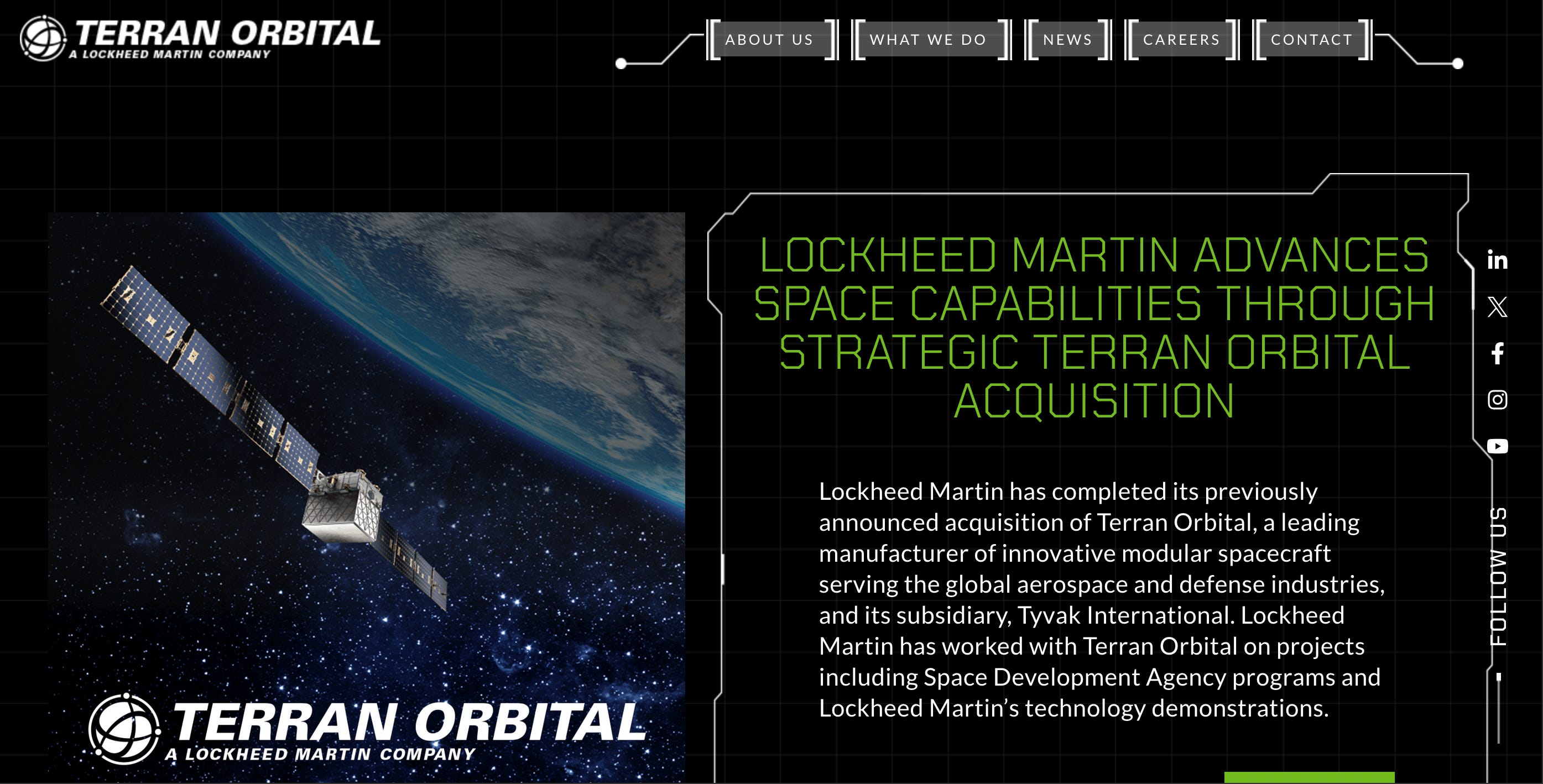

Terran Orbital – Strategic-Technological Analysis

Terran Orbital Corporation, a satellite manufacturer founded in 2013 and now part of Lockheed Martin, has rapidly emerged as a leader in small satellite technology for aerospace and defence[1][2]. Its end-to-end approach – from modular spacecraft design and production to mission operations – powers constellations and space missions worldwide. The company’s Italian subsidiary, Tyvak International, is increasingly involved in European space programmes (ESA and national projects) aimed at enhancing strategic autonomy. In Europe’s shifting security context, Terran’s satellites and services (e.g. on-orbit situational awareness, secure satellite communications, Earth imaging) are drawing attention as potential contributors to allied deterrence and resilience. This analysis delves into Terran Orbital’s technologies, European engagements and gap areas from the perspective of EU/NATO objectives. By assessing its technology portfolio, participation in EU defence initiatives and alignment with strategic-autonomy goals, we illuminate how a U.S.-origin company can support Europe’s defence-tech ambitions while balancing transatlantic integration.